In March 2025, Representatives Tom Suozzi and John Moolenaar introduced the Well-Being Insurance for Seniors to be at Home Act, commonly called the WISH Act. It is the most serious federal long-term care legislation in years. It has bipartisan support. A Morningstar study found it would cut retirement shortfall rates for single women from 58% to 28%.

It would also, if passed, leave most South Florida families with a coverage gap large enough to devastate their savings.

Understanding what the WISH Act actually does, and what it deliberately does not do, is one of the most important planning conversations happening right now. This article covers both.

What the WISH Act Actually Is

The WISH Act would create a federal catastrophic long-term care insurance program modeled partly on Social Security. Workers and employers would each contribute 0.3% of wages to a Long-Term Care Insurance Trust Fund. After a qualification period of six quarters of coverage, eligible individuals who develop a qualifying disability would receive a monthly benefit to help pay for care.

The initial monthly benefit would start at approximately $3,600 and adjust with inflation over time. The benefit is specifically designed to help people stay at home rather than enter a nursing facility, which aligns with what most seniors actually want.

A federal monthly benefit of approximately $3,600 (inflation-adjusted over time) for seniors who:

- Have contributed to the program for at least six quarters

- Have a qualifying disability affecting activities of daily living

- Have completed the elimination period based on their income level

The program is designed to reduce seniors' need to spend down assets to qualify for Medicaid, reduce the burden on family caregivers, and make private LTC insurance more affordable by reducing the catastrophic tail risk that drives carrier pricing.

The Part Most Articles Skip: The Elimination Period

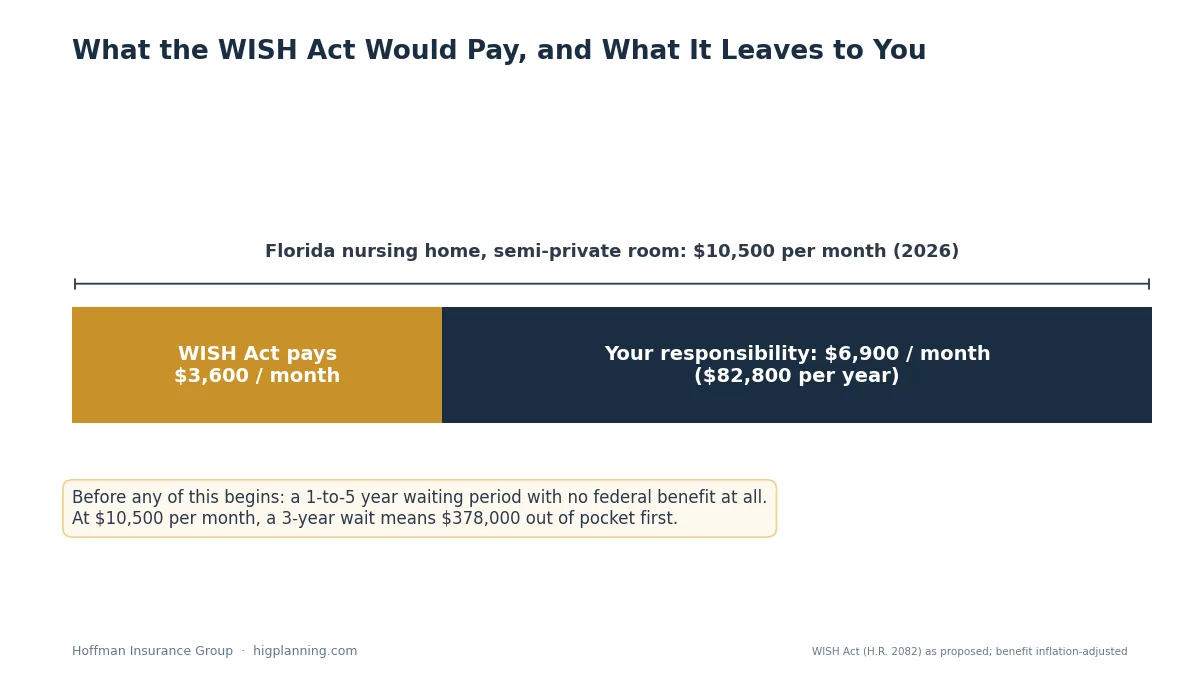

The WISH Act has a 1 to 5 year elimination period, scaled by income. During that period, you are expected to cover your own care through private insurance or personal savings. The federal benefit does not begin until after you have been paying for care yourself.

This is not a design flaw. It is intentional. The legislation is specifically structured to be fiscally sustainable and to avoid the adverse selection problems that killed earlier federal LTC proposals. It covers catastrophic, long-duration care. The early period of care is yours to finance.

Now look at what that means in Florida.

What Long-Term Care Actually Costs in Florida Right Now

Florida's long-term care costs in 2026 are among the highest in the Southeast. The state's aging population, strong demand for care, and higher cost of living in South Florida specifically push costs well above national medians in many markets.

The average length of a nursing home stay in Florida is two to three years. At $10,000 per month for three years, the total cost is $360,000. At $12,000 per month, it is $432,000.

Most families' savings are depleted within the first year of nursing home care unless a plan is in place.

Running the Numbers: What the Gap Actually Looks Like

Take a middle-income Florida household. They have a 3-year elimination period under the WISH Act based on their income. They need nursing home care at $10,500 per month.

Months 1 through 36: Private pay at $10,500/month. Total out-of-pocket before federal benefit begins: $378,000.

Month 37 onward: WISH Act benefit kicks in at $3,600/month. Remaining cost per month: $10,500 minus $3,600 equals $6,900 still owed privately.

The federal program reduces the ongoing cost. It does not eliminate the elimination period, and it does not cover the full monthly bill even after it starts.

For a family without private LTC insurance, the elimination period alone can consume most of a retirement portfolio.

This gap is not an oversight. The WISH Act was designed to work alongside private insurance, not replace it. The legislation's own sponsors have said that one of its goals is to make private LTC insurance more affordable by reducing the tail risk that makes carriers cautious. Private coverage handles the elimination period and fills the remaining monthly gap. Federal coverage handles the catastrophic long-duration tail.

Three More Problems With Waiting

The Bill Has Not Passed

The WISH Act was introduced in March 2025 and reintroduced in the 119th Congress. It has genuine bipartisan support, which is notable. It has not passed. Federal LTC legislation has been introduced, debated, and withdrawn multiple times since the 1980s. The most recent serious attempt, the CLASS Act included in the Affordable Care Act in 2010, was withdrawn before implementation because it was not actuarially sound.

The WISH Act is more carefully designed than the CLASS Act. It may eventually pass. But planning around legislation that does not yet exist is a risky strategy for something as consequential as long-term care financing.

Today's 55-Year-Old Would Contribute for Years Before Qualifying

The program requires six quarters of coverage to qualify. Someone who is 55 today and begins contributing when the program starts would potentially contribute for a decade or more before needing benefits. Meanwhile, their health status changes. Private LTC insurance purchased at 55 locks in the rates and underwriting of a 55-year-old. Private LTC insurance purchased at 65 or 70, if the person can still qualify, costs significantly more and may have exclusions that did not exist a decade earlier.

The Private LTC Market Is Shrinking

The number of carriers offering standalone traditional LTC policies has declined sharply over the past two decades. Where more than 100 companies were selling policies in 2002, roughly a dozen were actively selling meaningful standalone coverage by the early 2020s. Some carriers that had exited filed new products in 2025, which is a positive development. But the market is tighter than it was, and underwriting standards have tightened with it.

Hybrid life and LTC combination products have filled part of the gap and are now the leading private LTC solution, according to a joint LIMRA and EY survey published in January 2026. These products combine a life insurance or annuity base with LTC acceleration benefits, which addresses the concern many people have about paying premiums for decades and never filing a claim. If you never need LTC, your heirs receive a death benefit.

Standalone traditional LTC: Only a handful of carriers still actively sell meaningful individual policies. Premiums are tax-deductible. Benefits are substantial per premium dollar. Rates can increase over time.

Hybrid life/LTC: Several major carriers offer combination products. No use-it-or-lose-it concern. Premium increases are generally locked. Less benefit per dollar than standalone, but meaningful LTC coverage alongside a death benefit.

Annuity-based LTC: Converts existing savings into a guaranteed LTC fund. Can qualify without new medical underwriting in some cases. Useful for those with existing assets to reposition.

How Florida's Demographics Make This More Urgent

Approximately 21.3% of Florida's population is 65 or older, one of the highest percentages in the country. South Florida specifically has significant concentrations of retirees and pre-retirees with meaningful assets to protect.

That demographic reality has two implications for LTC planning. First, demand for care in South Florida is high and rising, which keeps costs elevated. Second, the people around you who need care are visible in a way they are not in younger markets. Many South Florida families have already watched a parent or grandparent go through the financial destruction of unplanned long-term care costs. The experience of seeing what happens without a plan tends to change how urgently people approach their own planning.

What Medicare and Medicaid Actually Cover

This is worth stating directly because confusion about it is extremely common.

Medicare does not cover long-term custodial care. It covers up to 100 days of skilled nursing facility care following a qualifying hospital stay. After 100 days, Medicare coverage ends entirely. The nursing home bills continue.

Medicaid covers long-term care for people who qualify financially. In Florida in 2026, qualifying for Medicaid LTC requires monthly income below $2,982 and assets below $2,000. The community spouse resource allowance, the amount a healthy spouse can keep, is $162,660. For many South Florida families with retirement savings, a home, and investment accounts, the Medicaid path requires spending down most of what they have worked to accumulate.

Medicaid is a genuine safety net and it serves many Floridians well. But qualifying for it requires depleting most of your assets first. The $2,000 asset limit for individuals means that a family with a $500,000 retirement account must generally spend most of that account on care before Medicaid begins covering costs.

Medicaid planning with an elder law attorney can protect some assets through legal strategies. But the planning works best when it starts years before care is needed, not when a crisis is already happening. And the most effective strategy for preserving wealth is usually a combination of early private insurance and proper estate planning, not Medicaid planning alone.

The Right Planning Framework

Long-term care planning is not a single product decision. It is a financial planning question that involves your age, health, assets, family situation, and risk tolerance. The right answer varies significantly by person.

| Profile | Primary Consideration | Recommended Starting Point |

|---|---|---|

| Ages 50 to 60, good health, meaningful assets | Best time to act. Rates are lowest, underwriting most favorable. | Standalone LTC or hybrid life/LTC policy |

| Ages 60 to 70, still insurable | Window is narrowing. Health changes can affect eligibility. | Hybrid or annuity-based product. Review standalone options. |

| Ages 70+, health concerns | Traditional underwriting may be difficult. Options exist but are more limited. | Annuity-based LTC. Elder law planning. Asset protection strategies. |

| Business owners with excess cash | Tax-advantaged structures available. Can integrate with business planning. | Hybrid life/LTC or annuity-based. Consult tax advisor. |

| High-net-worth, self-insuring consideration | Self-insuring LTC works if assets exceed $2M to $3M. Below that, insurance is usually more efficient. | Run the numbers. Self-insurance is legitimate but requires honest asset analysis. |

What to Do Right Now, Regardless of What Happens with the WISH Act

Whether the WISH Act passes next year or never passes, these three steps make sense for most South Florida families in their 50s and 60s.

Get a realistic cost estimate for care in your area. The numbers in this article are statewide medians. Nursing home costs in Fort Lauderdale, Boca Raton, and Coral Gables are higher. Know what you are actually planning for.

Check your insurability now. LTC underwriting considers your current health. Conditions that develop over the next five years may affect your ability to qualify for coverage. The only way to know your current options is to go through underwriting now.

Understand what your existing plan covers. Many people assume Medicare will handle long-term care. Many assume they will self-insure but have not calculated what that actually requires. A clear-eyed review of your current financial picture, your likely care costs, and your insurance options takes about 20 minutes and often changes the conversation significantly.